It represents the incremental money generated for each product/unit sold after deducting the variable portion of the firm’s costs. Refer to panel B of Figure 5.7 as you read Susan’s comments about the contribution how to make an invoice with xero margin income statement. A traditional income statement is prepared under a traditional absorption costing (full costing) system and is used by both external parties and internal management.

How do you calculate the contribution margin from EBIT?

On the other hand, variable costs are costs that depend on the amount of goods and services a business produces. The more it produces in a given month, the more raw materials it requires. Likewise, a cafe owner needs things like coffee and pastries to sell to visitors.

Products

The same will likely happen over time with the cost of creating and using driverless transportation. In the absorption and variable costing post, we calculated the variable product cost per unit. The contribution margin income statement is a very useful tool in planning and decision making. While it cannot be used for GAAP financial statements, it is often used by managers internally. Fixed costs are costs that are incurred independent of how much is sold or produced.

Calculating Your Contribution Margin

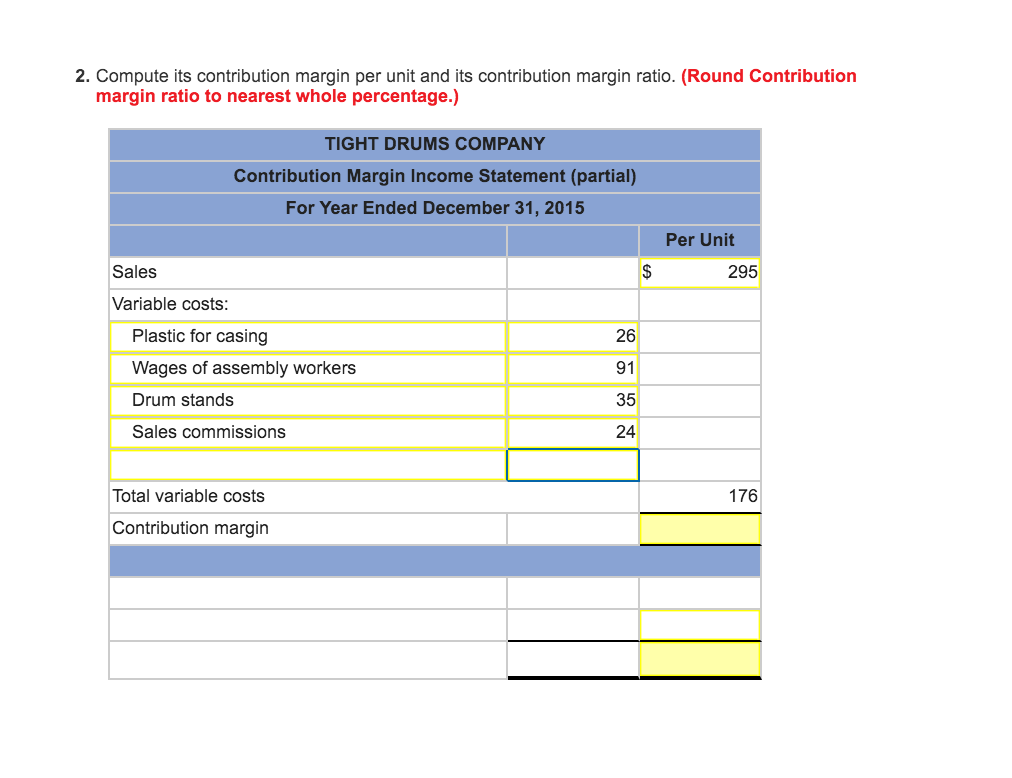

Another income statement format, called the contribution margin income statement11 shows the fixed and variable components of cost information. Note that operating profit is the same in both statements, but the organization of data differs. The contribution margin income statement organizes the data in a way that makes it easier for management to assess how changes in production and sales will affect operating profit. The contribution margin12 represents sales revenue left over after deducting variable costs from sales. It is the amount remaining that will contribute to covering fixed costs and to operating profit (hence, the name contribution margin). The Contribution Format Income Statement, also known as the variable costing income statement, is a financial report that separates costs into fixed and variable costs.

- An effective tax rate is a rate used if the company applied the same tax rate consistently over the accounting period.

- A contribution income statement is a powerful tool in accounting and finance, providing valuable insights into a company’s financial performance.

- Last month, Alta Production, Inc., sold its product for $2,500 per unit.

- Very low or negative contribution margin values indicate economically nonviable products whose manufacturing and sales eat up a large portion of the revenues.

- When preparing internal reports on theperformance of segments of a company, management often finds it isimportant to classify expenses as fixed or variable and as director indirect to the segment.

Fixed costs remained unchanged; however, as more units are produced and sold, more of the per-unit sales price is available to contribute to the company’s net income. In our example, the sales revenue from one shirt is \(\$15\) and the variable cost of one shirt is \(\$10\), so the individual contribution margin is \(\$5\). This \(\$5\) contribution margin is assumed to first cover fixed costs first and then realized as profit. This covers the product costs, but remember we must include all the variable costs. The contribution margin is the foundation for break-even analysis used in the overall cost and sales price planning for products.

The Difference Between a Contribution Margin Income Statement and a Normal Income Statement

This makes the EBITDA figure important for investors looking to put money into a business. A contribution margin is a narrow view of a product or service’s profitability, but the net profit is a much wider and more comprehensive look at a company’s financial performance. An income statement would have a much more detailed breakdown of the variable and fixed expenses. It’s important to note this is a very simplified look at a contribution margin income statement format. Some other examples of fixed costs are equipment and machinery, salaries that aren’t directly related to the product’s manufacturing, and fixed administrative costs. It is important to note that this unit contribution margin can be calculated either in dollars or as a percentage.

EBIT provides an overall view of the company’s profitability level, whereas contribution margin looks at the profitability of each individual service or product. EBIT features in a company income statement as it gives the operating figures of a business more context. The contribution margin provides the profitability of each individual dish at a restaurant, whereas income would look at the entire restaurant’s overall financial health. Let’s say that our beauty conglomerate sells 1,000 units of its bestselling skincare products for $50 each, totaling $50,000 in revenue.

Buying items such as machinery is a typical example of a fixed cost, specifically a one-time fixed cost. Regardless of how much it is used and how many units are sold, its cost remains the same. However, these fixed costs become a smaller percentage of each unit’s cost as the number of units sold increases. This is the net amount that the company expects to receive from its total sales.

While the contribution format sorts costs by whether they are variable or fixed, a traditional income statement separates costs by whether they are tied to production or not. These include the cost of goods sold (COGS) as well as selling, general, and administrative costs (SG&A). The two expense categories may contain both fixed and variable costs, which is why it can be useful to separate them using a contribution format statement. For the month of April, sales from the Blue Jay Model contributed \(\$36,000\) toward fixed costs. Looking at contribution margin in total allows managers to evaluate whether a particular product is profitable and how the sales revenue from that product contributes to the overall profitability of the company.